By Carter James | Oplexa Insights

April 2026 | 18 Min Read

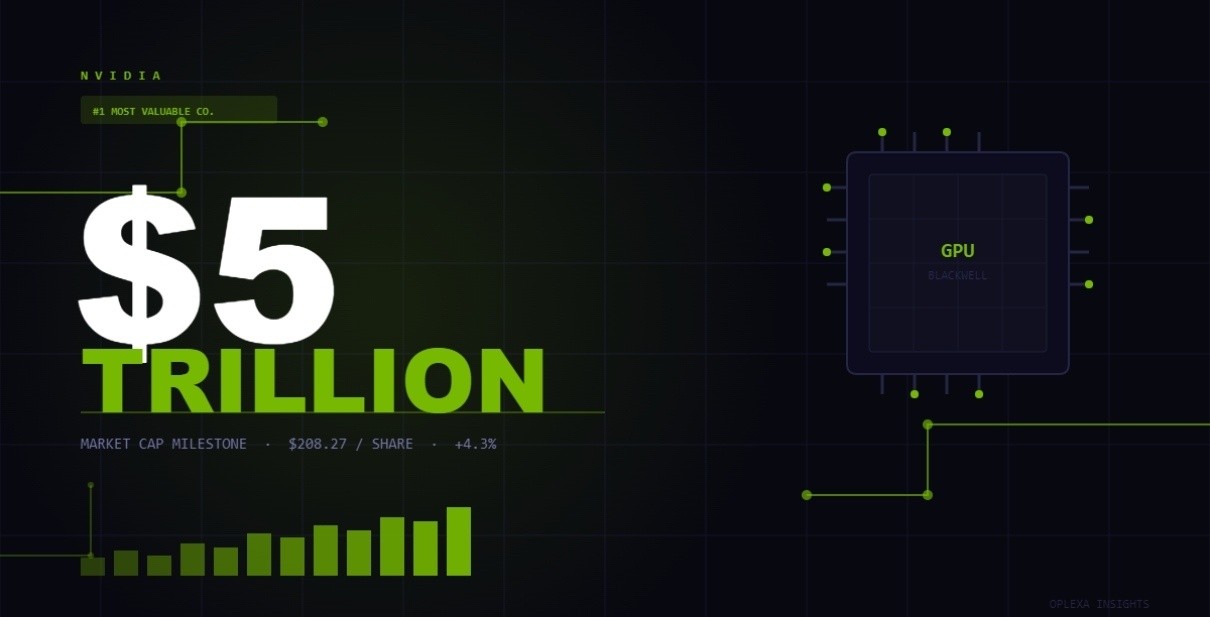

On April 24, 2026, NVIDIA’s $5 trillion market cap became a reality — the first semiconductor company in history to cross this threshold. Shares closed at a record $208.27, up 4.3%, pushing NVIDIA past Apple and Microsoft to become the world’s most valuable publicly traded company. The milestone added more than $200 billion in market value in a single session.

But this is not just a number. The NVIDIA $5 trillion market cap milestone lands at one of the most consequential weeks in AI chip investing history — with four of NVIDIA’s largest customers (Microsoft, Amazon, Google, Meta) reporting Q1 2026 earnings on April 29, a Federal Reserve decision on April 30, and a production cut to the Vera Rubin GPU already quietly circulating among institutional analysts.

This is Oplexa’s complete breakdown: what drove the NVIDIA $5 trillion market cap, what Intel’s 24% single-day surge signals about the broader semiconductor rally, what the bear case actually looks like at this valuation, and the three catalysts that will determine whether this milestone holds or retreats heading into May.

Key Numbers — April 24, 2026 Semiconductor Rally

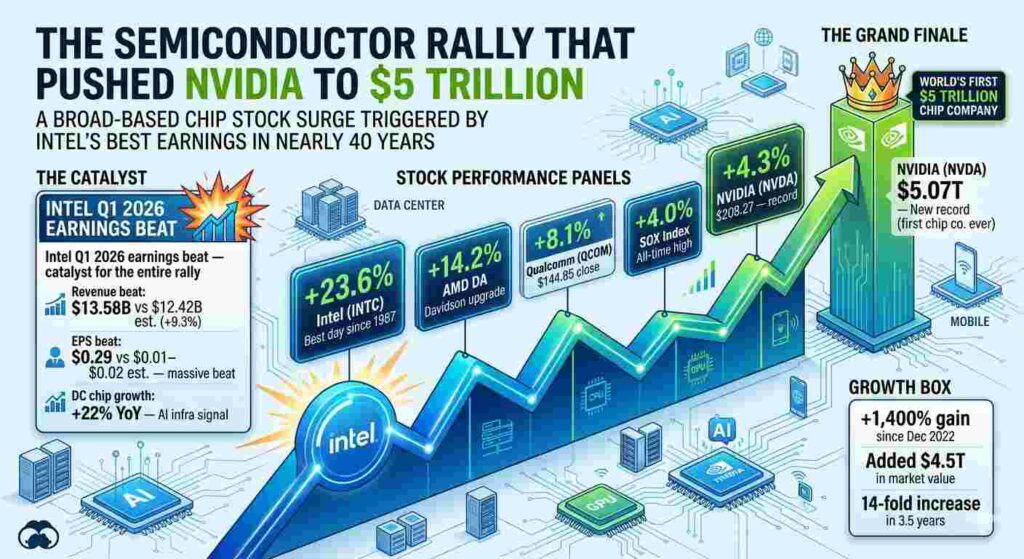

NVDA: +4.3% → $208.27 (record close) | Market Cap: $5.075T

INTC: +23.6% → Best day since 1987 | Q1 Revenue: $13.58B (beat by 9.3%)

AMD: +14% → $349.54 | QCOM: +8% → $144.85

SOX Index: +4% → All-time high | Nasdaq April return: +15% (best since April 2020)

How NVIDIA Reached a $5 Trillion Market Cap — The Full Story

NVIDIA’s journey to a $5 trillion market cap is one of the most compressed wealth creation events in equity market history. Since December 2022, the stock has risen more than 1,400% — adding over $4.5 trillion in market value in roughly three and a half years. To put that in perspective: NVIDIA created the equivalent of two Apple companies from scratch in the time it takes most enterprises to complete a single data center buildout.

The catalyst for that run is straightforward: NVIDIA holds approximately 80–85% market share in AI training accelerators, and every major AI workload — from ChatGPT to Claude to Gemini — runs on NVIDIA H100, A100, or Blackwell GPUs. There is no credible at-scale alternative. That market position gives NVIDIA pricing power that no hardware company in history has sustained at this scale.

What Triggered the April 24 Record — Intel’s Surprise Earnings

The immediate catalyst for NVIDIA’s $5 trillion market cap milestone was not NVIDIA’s own numbers. It was Intel’s.

Intel reported Q1 2026 revenue of $13.58 billion — beating analyst estimates of $12.42 billion by 9.3% — with adjusted earnings per share of $0.29, against expectations of just $0.01–$0.02. Data center chip sales jumped 22% year-over-year. Intel’s stock surged 23.6%, its best single-day performance since October 1987.

For NVIDIA investors, Intel’s numbers were a proxy signal. When a company that had largely been excluded from the AI chip boom delivers 22% data center revenue growth, it confirms one thing: AI infrastructure demand is not concentrated in a single chip category. It is expanding across the entire semiconductor stack — GPUs, CPUs, networking, memory, and storage. That is structurally bullish for NVIDIA, which sits at the apex of that stack.

The 6-Month Consolidation That Preceded the Breakout

NVIDIA had briefly touched $5 trillion in late October 2025 before pulling back. The six months that followed were a period of consolidation — not collapse — as investors worked through questions about the sustainability of AI spending, tariff uncertainty related to the Iran conflict, and supply chain concerns about TSMC’s advanced packaging capacity.

The April breakout is not speculative momentum. NVIDIA’s $5 trillion market cap is underpinned by $700 billion in committed hyperscaler capex — Microsoft ($146B), Amazon ($200B), Meta ($115–135B), Google ($175–185B) — and a $1 trillion revenue forecast from Jensen Huang himself for the next two years. Those are not analyst projections. They are public commitments from NVIDIA’s largest customers.

📊 Oplexa Report: NVIDIA Strategic Inflection Analysis 2025–2035 — Full revenue model, Vera Rubin production timeline, competitive positioning vs AMD and custom ASICs, and 10-year investment thesis. $2,500 →

NVIDIA Stock Record 2026 — Three Reasons This Rally Is Different

Every NVIDIA rally since 2023 has raised the same skeptical question: is this sustainable, or a bubble waiting to burst? The NVIDIA stock record 2026 deserves a more nuanced answer than either pure bull or bear framing. Here are three reasons this particular breakout has structural legs that previous rallies lacked.

1. The Revenue Is Real — Not Forward Speculation

NVIDIA’s Blackwell GPU architecture — launched in H2 2024 — is generating revenue at a pace that has repeatedly exceeded even the most aggressive Wall Street estimates. In NVIDIA’s fiscal Q4 2026 (reported February 2026), data center revenue hit $35.6 billion — up 93% year-over-year. That is not projected revenue. That is booked revenue, invoiced, and collected from customers who have no viable alternative for large-scale AI training.

The NVIDIA stock record 2026 is not priced on “AI will be big someday.” It is priced on AI being enormous right now, with hyperscalers explicitly telling investors they will spend more on AI infrastructure in 2026 than in any prior year.

2. Jensen Huang’s $1 Trillion Revenue Call Is Credible

At GTC 2026 in March, Jensen Huang publicly forecast that NVIDIA would generate $1 trillion in revenue over the next two years. Wall Street’s consensus estimate sits below that figure. But consider the math: four hyperscalers are spending a combined $700 billion on AI infrastructure in 2026 alone. If NVIDIA captures even 25% of that spend — a conservative figure given its market share — that is $175 billion in annual revenue from four customers. Add enterprise, sovereign AI, and automotive, and $500 billion in annual revenue by fiscal 2028 is not implausible. The NVIDIA stock record 2026 reflects early-adopter institutional investors pricing in exactly this trajectory.

3. The AI Chip Stock Rally Has Broadened — That Is the Most Bullish Signal

Previous NVIDIA rallies were largely isolated — the stock moved on its own results and its own narrative. The AI chip stock rally 2026 is categorically different. On April 24, NVIDIA, Intel, AMD, Qualcomm, and the entire Philadelphia Semiconductor Index moved to all-time highs simultaneously. The SOX index gained 40.4% in April alone.

When a sector rallies this broadly, it signals that investors are not just buying NVIDIA — they are making a structural bet on the entire AI hardware ecosystem. That is a more durable foundation than a single-stock momentum trade.

Intel Earnings April 2026 — What the 24% Surge Actually Signals

Intel’s performance in the AI chip stock rally 2026 deserves its own analysis, because it changes the competitive narrative in a way that matters for NVIDIA investors.

For the past three years, the prevailing narrative was that Intel had been left behind by the AI revolution — a CPU-centric company in a GPU-dominated world. Intel’s April 2026 earnings complicate that story in important ways.

Data Center CPU + AI — Intel’s Actual Q1 2026 Numbers

- Q1 2026 Revenue: $13.58 billion — 9.3% above consensus of $12.42B

- Adjusted EPS: $0.29 — versus analyst expectation of $0.01–$0.02

- Data center chip revenue: +22% year-over-year

- Intel Gaudi AI accelerator sales: growing — but still small relative to NVIDIA

- Stock reaction: +23.6% — best single-day performance since October 1987

The 22% data center growth is the critical number from Intel’s April 2026 earnings. It signals that AI infrastructure buildout is driving CPU demand alongside GPU demand — enterprises are not just buying GPUs in isolation. Every AI training cluster needs server CPUs, networking chips, and memory controllers. Intel’s data center business benefits from all of these adjacencies even without winning GPU market share.

Does Intel Compete With NVIDIA — Or Complement It?

The short answer: both, depending on workload. Intel’s Gaudi AI accelerators target inference-at-scale use cases where cost efficiency matters more than peak training performance — a segment where NVIDIA’s Blackwell and Vera Rubin are arguably overspecified. The Intel earnings April 2026 results suggest Gaudi is gaining traction, but NVIDIA’s GPU dominance in frontier model training remains effectively unchallenged.

For investors, the more important Intel story from Intel earnings April 2026 is what it signals about AMD: if Intel — which has been structurally disadvantaged in AI for three years — can grow data center revenue 22% year-over-year, what does that imply for AMD’s Q1 results, due April 29?

NVIDIA vs AMD 2026 — Where the Real Competition Is

The NVIDIA vs AMD 2026 competitive dynamic is more nuanced than most coverage suggests. AMD surged more than 14% on April 24 alongside NVIDIA — DA Davidson upgraded AMD the same day, calling it a primary beneficiary of AI infrastructure expansion. That reaction tells you something important about how the semiconductor market cap 2026 story is evolving.

Where AMD Is Actually Winning

AMD’s MI300X and MI325X GPUs have secured meaningful design wins at Microsoft Azure and Google Cloud — not as primary training chips, but as inference-optimized alternatives for specific workloads. Meta is committed to deploying up to 6 gigawatts of AMD GPUs in 2026 — a significant volume commitment that confirms AMD’s position as NVIDIA’s most credible at-scale alternative.

In the NVIDIA vs AMD 2026 comparison, the key differentiator is not raw benchmark performance — NVIDIA still leads on most training metrics. It is software ecosystem lock-in. NVIDIA’s CUDA platform has a 15-year head start and a developer ecosystem of millions. AMD’s ROCm software stack has improved significantly, but enterprises building production AI infrastructure in 2026 still default to CUDA-native toolchains. Switching costs are real and quantifiable.

Where NVIDIA’s Moat Is Weakest

The most credible threat to NVIDIA in the NVIDIA vs AMD 2026 dynamic is not AMD directly — it is custom ASICs. Google’s TPU v8 (Sunfish for training, Zebrafish for inference), Amazon’s Trainium 3, and Meta’s MTIA are all designed to displace NVIDIA GPUs for specific high-volume internal workloads. These are not external products — they are captive chips designed for single customers. But at hyperscaler scale, even partial displacement is significant: if Google runs 30% of its AI inference on TPU v8 instead of NVIDIA GPUs, that is a multi-billion-dollar annual revenue hole for NVIDIA at its largest customer.

This is the structural risk that the NVIDIA $5 trillion market cap embeds but does not fully price. Custom ASIC market share is growing — our Custom ASIC Market 2026 analysis projects the ASIC market will reach $118 billion by 2033, up from $15 billion in 2023.

The Bear Case at $5 Trillion — Three Real Risks

No analysis of the NVIDIA $5 trillion market cap milestone is complete without engaging seriously with the bear case. At this valuation, three risks warrant attention from advanced investors.

Risk 1: Vera Rubin Production Cut

KeyBanc Capital Markets estimates NVIDIA has cut its 2026 Vera Rubin GPU production target from 2 million units to 1.5 million — a 25% reduction — due to HBM4 memory certification delays at SK Hynix and Micron. Vera Rubin server rack forecasts were cut more sharply: from 12,000–14,000 units to approximately 6,000 units. This directly affects NVIDIA’s revenue trajectory for H2 2026 and pushes Jensen Huang’s $1 trillion revenue call further into 2027. Investors pricing in peak Vera Rubin volumes in fiscal 2027 may be working with inflated assumptions.

Risk 2: SOX Index Overbought — RSI Near 85

The Philadelphia Semiconductor Index’s deviation from its 200-day moving average is at the highest level since June 2000. The SOX RSI briefly hit 85 on April 24 — well into extreme overbought territory. ZeroHedge noted that positioning, fund flows, and volatility are all chasing the same direction: “This is no longer a pure AI bull market but a liquidity-driven AI chasing game.” Corrections from this technical setup can be sharp — the question is whether fundamental demand absorbs selling pressure or amplifies it.

Risk 3: Hyperscaler Earnings Guidance Risk — April 29

On April 29, Microsoft, Amazon, Google, and Meta will report Q1 2026 results simultaneously. For the NVIDIA $5 trillion market cap to hold, all four must reaffirm their 2026 AI infrastructure spending guidance. Even a single major hyperscaler trimming capex guidance by 10–15% would hit NVIDIA disproportionately — the stock would price in a demand shortfall across all four customers. The setup is high-reward if guidance holds, high-risk if any hyperscaler blinks.

Semiconductor Market Cap 2026 — The Broader Landscape

NVIDIA’s $5 trillion market cap does not exist in isolation. The semiconductor market cap 2026 context shows an industry at a structural inflection point that extends well beyond a single company’s valuation.

The global semiconductor market is on track to approach $1 trillion in annual revenue in 2026 — a third consecutive year of double-digit growth. That growth is heavily concentrated in AI-specific categories: logic (advanced GPUs, custom ASICs), HBM memory, and advanced packaging. Traditional categories — consumer electronics, automotive, industrial — remain mixed.

The semiconductor market cap in 2026 reflects this concentration. NVIDIA alone represents approximately 20% of the S&P 500’s 4.7% year-to-date gain. The iShares Semiconductor ETF (SOXX) is up 40.4% in April 2026 alone. Broadcom — which holds custom ASIC design partnerships with both Google and Meta — has gained 10% year-to-date and is now being valued as a structural beneficiary of the hyperscaler custom chip shift.

The structural insight for investors evaluating the semiconductor market cap 2026 landscape: AI chip demand is not a winner-take-all market. Intel’s 22% data center growth, AMD’s Meta design win, and Broadcom’s dual hyperscaler partnerships all confirm that the AI infrastructure buildout is creating multi-hundred-billion-dollar revenue pools that support multiple winners simultaneously.

📊 Oplexa Report: AI Chip Market Analysis & Forecast 2025–2035 — Full competitive landscape, market share projections by chip category, NVIDIA vs AMD vs custom ASIC revenue models, and 10-year institutional investment framework. $1,499 →

What Happens Next — Three Scenarios for NVIDIA After $5 Trillion

Advanced investors need more than milestone coverage. Here are the three most probable scenarios for the NVIDIA $5 trillion market cap following the April 24 breakout, based on the catalysts materializing this week.

Scenario 1 — Bull Case: Hyperscalers Reaffirm Spending (Probability: 65%)

Microsoft, Amazon, Google, and Meta all reaffirm or raise 2026 AI infrastructure capex guidance on April 29. The Fed holds rates steady at 3.50–3.75% with neutral tone on May 1. Vera Rubin production cut is disclosed but framed as timing, not demand. NVIDIA stock consolidates at $200–$215 through May 20 earnings, then breaks higher on confirmed Q1 FY2027 results.

NVIDIA price target in this scenario: $220–$240 by end of June 2026.

Scenario 2 — Base Case: Mixed Signals, Consolidation (Probability: 25%)

At least one hyperscaler trims capex guidance marginally. Fed tone is hawkish. Vera Rubin production cut is widely reported in institutional research. NVIDIA corrects 10–15% from the $208 close but holds the 200-day moving average. SOX index pulls back from overbought RSI. AI chip investment thesis remains intact but near-term momentum fades.

NVIDIA range in this scenario: $175–$195 through May 2026.

Scenario 3 — Bear Case: Hyperscaler Guidance Miss (Probability: 10%)

A major hyperscaler — most likely Microsoft or Amazon — explicitly reduces 2026 AI infrastructure spending guidance citing macro uncertainty from Iran conflict escalation or tariff pressure. This triggers a cascade sell-off across semiconductor stocks from technically overbought levels. The NVIDIA $5 trillion market cap milestone proves a local top.

NVIDIA downside in this scenario: $155–$170, representing a 18–25% correction from the April 24 close. Still above January 2026 lows, but a significant mark-to-market impact for investors who entered at record levels.

What Advanced Investors Should Do Right Now

The NVIDIA $5 trillion market cap milestone is not an entry or exit signal on its own. Here is what advanced investors should focus on in the next 72 hours.

Watch hyperscaler capex guidance language carefully. The specific phrase to look for in Microsoft’s April 29 earnings call is whether management reaffirms their $146 billion AI/cloud capex figure or hedges with language like “we are evaluating the pace of deployment.” Any hedging language on capex — even with overall spending held flat — will be read as a demand signal for NVIDIA and will move the stock.

Track SK Hynix HBM4 certification timelines. The Vera Rubin production cut is directly tied to HBM4 yield maturity at SK Hynix and Micron. Any update from SK Hynix — which reports earnings this week — on HBM4 certification timelines will affect Vera Rubin volume estimates for H2 2026. Our AI Memory Semiconductor analysis covers the HBM4 supply chain in detail.

Monitor the SOX/NVDA spread. When NVDA underperforms the SOX index on a down day — meaning semiconductor stocks pull back broadly but NVIDIA pulls back more — it signals institutional rotation out of the single largest position. The April rally showed NVIDIA underperforming the SOX on the upside (19% vs 40.4% for SOXX in April). That divergence can flip quickly when sentiment shifts.

Conclusion

The NVIDIA $5 trillion market cap milestone on April 24, 2026 is historically significant for a single reason: no semiconductor company has ever been here before. Apple and Microsoft crossed this threshold as software and platform businesses — companies where marginal cost approaches zero and revenue scales with users. NVIDIA crossed it as a hardware company, where every dollar of revenue requires a GPU to be designed, manufactured, packaged, and shipped.

That distinction matters. The NVIDIA $5 trillion market cap is supported by real physical demand — $700 billion in hyperscaler capex, 80%+ GPU market share in AI training, and a customer base that has no viable near-term alternative for large-scale model development. It is also exposed to real physical constraints — HBM4 certification delays, TSMC packaging capacity limits, and power infrastructure bottlenecks covered in our AI Data Center Power Crisis analysis.

The semiconductor rally that delivered the NVIDIA $5 trillion market cap milestone is not a bubble. It is a compressed valuation of a decade-long AI infrastructure buildout, being priced in real time by a market that — for once — is ahead of the news rather than behind it. What happens next depends on whether the infrastructure investment commitments hold. As of April 27, 2026, all signals point toward they do — but the next 72 hours will be the most rigorous test of that thesis in six months.

Frequently Asked Questions

How did NVIDIA reach a $5 trillion market cap?

NVIDIA reached a $5 trillion market cap on April 24, 2026, when shares surged 4.3% to a record $208.27. The immediate catalyst was Intel’s Q1 2026 earnings beat — revenue of $13.58 billion against estimates of $12.42 billion, with data center chip sales up 22% year-over-year — which sparked a broad AI chip stock rally. The underlying driver is NVIDIA’s 80–85% market share in AI training GPUs, backed by $700 billion in committed 2026 hyperscaler capex from Microsoft, Amazon, Google, and Meta. NVIDIA has gained more than 1,400% since December 2022 — adding over $4.5 trillion in market value.

Is NVIDIA stock a buy, sell, or hold at $5 trillion market cap?

At the $5 trillion market cap level, most institutional analysts rate NVIDIA a hold-to-buy, with price targets ranging $220–$260 for the next 12 months. The bull case: $700B hyperscaler capex, $1T revenue forecast from Jensen Huang, and no credible GPU alternative at scale. The bear case: Vera Rubin production cut from 2M to 1.5M units due to HBM4 certification delays, SOX RSI near 85 (historically overbought), and hyperscaler earnings guidance risk on April 29. Advanced investors should wait for hyperscaler Q1 earnings clarity before making new position decisions at record prices.

What did Intel’s Q1 2026 earnings show?

Intel’s Q1 2026 earnings showed revenue of $13.58 billion — 9.3% above analyst estimates — with adjusted EPS of $0.29 versus expectations of $0.01–$0.02. Data center chip sales jumped 22% year-over-year. The results triggered Intel’s best single-day stock performance since 1987, with shares surging 23.6%. The numbers confirmed AI infrastructure demand is expanding beyond GPU-specific categories into CPUs, networking, and storage — a structurally bullish signal for the entire semiconductor sector.

How does NVIDIA’s $5 trillion market cap compare to other companies?

NVIDIA’s $5 trillion market cap makes it the world’s most valuable company, surpassing Apple ($4.1 trillion) and Microsoft ($3.2 trillion). NVIDIA is worth $1 trillion more than the second-largest company, Alphabet. Only Apple and Microsoft have previously crossed $5 trillion — both took decades. NVIDIA crossed it in approximately three and a half years, driven entirely by AI infrastructure demand. No semiconductor company has ever reached this valuation milestone before NVIDIA.

What is the NVIDIA Vera Rubin production cut and why does it matter?

KeyBanc Capital Markets estimates NVIDIA cut its 2026 Vera Rubin GPU production target from 2 million to 1.5 million units — a 25% reduction — due to HBM4 memory certification delays at SK Hynix and Micron. Vera Rubin server rack forecasts were cut from 12,000–14,000 units to approximately 6,000. This pushes NVIDIA’s peak H2 2026 revenue catalyst into 2027 and creates near-term earnings risk heading into May 20 fiscal Q1 FY2027 results. Investors pricing peak Vera Rubin volumes into current FY2027 estimates may be working with inflated numbers.

Will the AI chip stock rally continue after NVIDIA’s $5 trillion milestone?

The continuation depends primarily on hyperscaler Q1 2026 earnings from Microsoft, Amazon, Google, and Meta on April 29. If all four reaffirm $700 billion+ combined 2026 capex, the rally has fundamental support despite the SOX index’s overbought RSI near 85. If any major hyperscaler trims AI infrastructure spending guidance — even marginally — the technical setup creates meaningful downside risk. The structural AI demand thesis remains intact through 2028, but near-term valuation at all-time highs requires execution confirmation from the four companies that are NVIDIA’s largest customers.

Related Oplexa Coverage:

- NVIDIA Vera Rubin GPU: Complete Platform Guide for H2 2026 — The Vera Rubin production cut context and full architecture analysis

- Custom ASIC Market 2026: Why Hyperscalers Are Ditching NVIDIA — The structural long-term risk to NVIDIA’s $5 trillion market cap

- AI Data Center Power Crisis 2026: Why $660B Capex Still Isn’t Enough — Infrastructure constraints that cap NVIDIA’s addressable market growth

- Micron’s $25B Bet: Why AI Memory Is the Next Semiconductor Gold Rush — HBM4 supply chain — the bottleneck causing the Vera Rubin production cut

- GTC 2026 Wrap-Up: Every NVIDIA Announcement That Will Define AI in 2027 — Full context behind NVIDIA’s $1 trillion revenue forecast

📊 Oplexa Report: NVIDIA Strategic Inflection Analysis 2025–2035 — $2,500

Full Vera Rubin production model, 10-year revenue projections, competitive positioning vs AMD and custom ASICs, hyperscaler capex sensitivity analysis, and institutional investment framework through 2035.

📊 Oplexa Report: AI Chip Market Analysis & Forecast 2025–2035 — $1,499

Full semiconductor market cap projections, NVIDIA vs AMD vs custom ASIC market share model, GPU pricing trajectory, and AI chip investment thesis for institutional allocators.