By Carter James | Oplexa Insights

May 2026 | 18 Min Read

Broadcom AI revenue 2026 is the single most important data point in the custom AI chip market right now. In Q1 fiscal 2026, Broadcom posted $8.4 billion in AI semiconductor revenue — up 106% year-over-year — and CEO Hock Tan declared “line of sight to achieve AI revenue from chips in excess of $100 billion in 2027.” That would make Broadcom’s AI chip business alone larger than the entire global semiconductor market was a decade ago.

But one week after that declaration, a complication surfaced. OpenAI’s $18 billion Project Nexus chip buildout with Broadcom hit a financing snag — with Microsoft reportedly refusing to provide the purchase guarantees needed to secure lender financing. The stock sold off. Bears called it a leading indicator of AI capex bubble risk. Bulls called it noise around Broadcom’s sixth-newest and smallest XPU customer.

Who is right? This is Oplexa’s complete analysis of Broadcom AI revenue 2026 — the Q1 numbers, the six-customer XPU pipeline, the math behind the $100 billion 2027 target, the OpenAI snag in full context, and what the Broadcom AI revenue 2026 trajectory means for AI infrastructure investors through 2028.

Broadcom AI Revenue 2026 — Q1 FY2026 Earnings in Full Context

Broadcom AI revenue 2026 in Q1 was not just a beat — it was a beat above Broadcom’s own forecast. CEO Hock Tan had projected a doubling of AI revenue entering 2026. The 106% year-over-year result exceeded that guidance, driven by what Tan described as “robust demand for custom AI accelerators and AI networking.” Total company revenue of $19.31 billion grew 29% year-over-year, beating the LSEG consensus of $19.18 billion.

The two-engine model Tan described — custom AI accelerators on one side, VMware enterprise software on the other — is running at full speed simultaneously. VMware software ARR is growing above 20% annually. Broadcom’s AI networking chips, which manage the high-speed interconnects inside AI data center clusters, are growing alongside XPU revenue. The AI infrastructure buildout requires both compute and networking — and Broadcom supplies both.

The Q2 FY2026 Guidance That Matters More Than Q1

For Broadcom AI revenue 2026 trajectory, the Q2 guidance of $10.7 billion is more important than the Q1 result. It implies sequential growth of 27% from Q1’s $8.4 billion — confirming that the XPU customer ramp is accelerating, not plateauing. At $10.7 billion in Q2, Broadcom AI revenue 2026 would hit an annualized run rate of $42.8 billion by mid-year. Tripling from $42.8 billion to $100 billion+ by end-2027 is aggressive but not implausible when the gigawatt math is applied to committed customers.

“We have line of sight to achieve AI revenue from chips, just chips, in excess of $100 billion in 2027. We have also secured the supply chain required to achieve this.” — Hock Tan, CEO Broadcom, Q1 FY2026 Earnings Call, March 4, 2026

📊 Oplexa Report: Custom ASIC Market 2026–2033: $118 Billion Opportunity — Full Broadcom competitive positioning, XPU customer pipeline analysis, market share projections vs AMD and Marvell, and 7-year investment thesis. $1,499 →

The Gigawatt Math — Why $100 Billion May Be Conservative

The most revealing exchange from Broadcom’s Q1 FY2026 earnings call was between CEO Hock Tan and Bernstein analyst Stacy Rasgon. Rasgon attempted to construct a bottom-up model for Broadcom AI revenue 2026 and 2027 using gigawatts as the unit of measurement — a framework that cuts through the uncertainty around exact customer volumes.

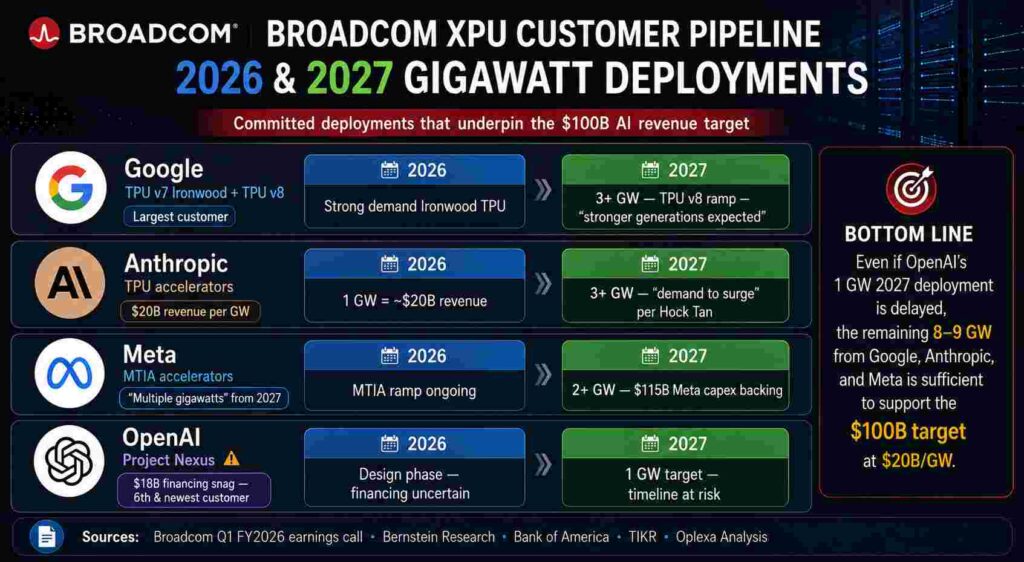

Rasgon’s math on Broadcom’s confirmed 2027 XPU commitments: Anthropic at 3+ gigawatts, OpenAI at approximately 1 gigawatt, Meta at 2+ gigawatts, Google at 3+ gigawatts — totaling 9–10 gigawatts across just these four named customers, before counting the two unnamed customers. Bank of America analyst Vivek Arya added the revenue-per-gigawatt estimate: Broadcom’s 2026 one-gigawatt deployment with Anthropic alone is expected to generate $20 billion in revenue. At $20 billion per gigawatt, 9–10 gigawatts of 2027 deployments implies $180–200 billion in potential AI revenue, making Hock Tan’s “$100 billion” guidance potentially conservative by design.

OpenAI Project Nexus — The $18 Billion Snag Explained

The most important context for understanding the OpenAI snag in the Broadcom AI revenue 2026 story is where OpenAI sits in Broadcom’s customer hierarchy: it is the sixth and newest customer. Not the first, not the largest, and not the one that anchors the $100 billion 2027 forecast.

What Happened

OpenAI and Broadcom had announced a custom AI chip partnership — code-named Project Nexus — designed to produce custom XPUs for OpenAI’s internal AI training and inference workloads. The first phase carries an $18 billion price tag. The complication: Microsoft — which has a significant financial relationship with OpenAI — refused to provide the purchase guarantees needed to secure lender financing for the $18 billion chip buildout. Without guaranteed purchase commitments, lenders are reluctant to commit capital to a program of this scale.

What It Actually Means for Broadcom AI Revenue 2026

CEO Hock Tan was explicit on the Q1 call: OpenAI is the sixth and newest customer, not the largest or most critical. The Project Nexus financing snag, if unresolved, affects future delivery timelines — not the AI revenue Broadcom is already guiding for in Q2 FY2026. Tan confirmed OpenAI’s first XPU deployment at 1 gigawatt is still expected in 2027. The snag creates timeline uncertainty, not a fundamental breakdown in the customer relationship.

For investors tracking Broadcom AI revenue 2026, the more important data point is what Tan said about the five other customers. For Google: “strong demand for the seventh-generation Ironwood TPU with even stronger generations expected in 2027.” For Anthropic: “off to a very good start in 2026 for one gigawatt of TPU compute,” with demand expected to “surge in excess of 3 gigawatts” in 2027. These two customers alone account for more than 4 gigawatts of 2027 committed deployments — enough to support significant progress toward the $100 billion target regardless of OpenAI’s timeline.

The Broader Risk the Snag Signals

The OpenAI financing snag is a symptom of a broader dynamic in AI infrastructure financing that investors should track. Nvidia has flagged a sharp rise in unpaid customer balances — receivables now sit near $33 billion as buyers take longer to settle invoices. Lenders are increasingly cautious that returns will not arrive on schedule. This does not invalidate the Broadcom AI revenue 2026 growth story — it suggests that the financing mechanics of the AI infrastructure buildout are becoming more complex as deal sizes scale toward tens of billions.

Broadcom’s Six XPU Customers — A Complete Breakdown

The Broadcom AI revenue 2026 thesis rests on six confirmed XPU customers. Understanding each customer’s contribution — and risk — is essential for evaluating whether the $100 billion 2027 target is achievable.

Customer 1 — Google (Largest, Most Stable)

Google is Broadcom’s original and largest XPU customer. Broadcom designs Google’s TPU accelerators — currently the TPU v7 Ironwood, with TPU v8 (Sunfish for training, Zebrafish for inference) already in development. On the Q1 call, Tan described “strong demand for the seventh-generation Ironwood TPU” with “even stronger generations expected in 2027 and beyond.” Alphabet has guided $175–185 billion in 2026 capex — nearly double 2025’s $91.4 billion. The majority of that is AI infrastructure spending that flows partially through Broadcom’s TPU design business.

Customer 2 — Anthropic (Fastest Growing)

Anthropic — which hit $30 billion ARR in April 2026 — is deploying 1 gigawatt of Broadcom-designed TPU capacity in 2026, with Hock Tan projecting demand surging “in excess of 3 gigawatts” in 2027. At Bank of America’s estimate of $20 billion revenue per gigawatt, Anthropic’s 2027 commitment alone represents $60+ billion in potential Broadcom AI revenue. Anthropic is the anchor customer for the $100 billion target — and its revenue trajectory, covered in our Google Cloud Next 2026 analysis, continues to accelerate.

Customer 3 — Meta (Multiple Gigawatts from 2027)

Meta’s MTIA (Meta Training and Inference Accelerator) program is “alive and well” per Hock Tan. Meta’s commitment to deploy multiple gigawatts of Broadcom-designed XPUs beginning in 2027 is backed by $115–135 billion in 2026 AI capex — the third-largest hyperscaler commitment globally. Meta’s partnership with Broadcom was extended through 2029, as covered in our Meta-Broadcom deal analysis.

Customers 4 & 5 — Two Unnamed (Apple and ByteDance Most Likely)

Two of Broadcom’s six XPU customers remain unnamed. Industry analysts — based on known ASIC development programs and Broadcom’s existing chip supply relationships — most frequently identify Apple and ByteDance as the candidates. Apple’s transition to custom silicon across all its platforms gives it both the engineering infrastructure and the economic motivation to develop XPUs for its AI server workloads. ByteDance’s scale as the world’s largest short-form video platform means inference economics are existential — custom silicon at this scale is commercially rational.

Customer 6 — OpenAI (Newest, Highest Risk)

OpenAI is the newest and, based on gigawatt commitments, smallest of Broadcom’s six XPU customers. The Project Nexus $18 billion financing snag creates near-term timeline uncertainty for the 1 gigawatt 2027 deployment. However, OpenAI’s total chip commitment — including the NVIDIA relationship, AMD partnership, and Amazon Trainium capacity — suggests the AI lab is diversifying across every major chip platform, with Broadcom as one of multiple options. OpenAI’s failure to close Broadcom financing would be a setback, not a catastrophe, for the Broadcom AI revenue 2026 and 2027 story.

📊 Oplexa Report: NVIDIA Strategic Inflection Analysis 2025–2035 — Full competitive analysis of Broadcom XPU vs NVIDIA GPU market share, custom ASIC displacement model, and 10-year investment framework. $2,500 →

Broadcom vs Marvell — The Emerging Custom ASIC Competition

The Broadcom AI revenue 2026 story exists alongside a competitive threat that deserves investor attention: Marvell Technology is aggressively expanding into custom silicon. Marvell is reportedly working with Alphabet on new AI chips while already supplying Amazon’s Trainium and Microsoft’s Maia processors. Broadcom currently commands approximately 70% of the custom AI accelerator market. Marvell’s multi-customer expansion — combined with Google’s addition of Marvell as a third chip design partner alongside Broadcom, as covered in our Google Cloud Next 2026 analysis — signals that hyperscalers are deliberately introducing competition into their custom chip supply chains.

For Broadcom, the Marvell threat is real but manageable on a 2026–2027 horizon. Broadcom’s 5+ years of XDSiP 3.5D packaging expertise, its established production relationships with TSMC, and the 15+ gigawatts of committed deployments in its pipeline create switching costs and timeline commitments that protect its near-term revenue base. The more serious medium-term risk is Google reducing Broadcom’s share of TPU design work as it diversifies to Marvell — a scenario that would not affect FY2027 revenues but could reshape the FY2028–2029 picture.

Apollo and Blackstone $35B Financing — What Private Credit Entering AI Signals

The most underreported element of the Broadcom AI revenue 2026 story is what Bloomberg reported alongside the earnings: Apollo and Blackstone are considering $35 billion in financing for Broadcom. This is private credit entering AI infrastructure financing at a scale that has no precedent.

The signal: institutional private credit managers — who have fiduciary obligations to their LPs and do not invest on hype — are confident enough in the Broadcom AI revenue 2026 growth trajectory and $100 billion 2027 target to consider $35 billion in financing commitments. This is not venture capital. Apollo and Blackstone manage combined AUM exceeding $1.5 trillion. When they consider a $35 billion commitment to a semiconductor company’s AI infrastructure buildout, it is a fundamental demand validation — not a speculative bet.

It also suggests that the OpenAI Project Nexus financing snag — where Microsoft refused purchase guarantees — is an isolated negotiating dispute, not a systemic breakdown in AI infrastructure financing confidence. Private credit is actively seeking exposure to AI infrastructure revenue streams at scale.

Is AVGO Stock a Buy? The Investor Framework

For investors evaluating Broadcom AI revenue 2026 as a stock thesis, three data points define the risk-reward:

Bull Case — $100B Is the Floor, Not the Ceiling

At $20 billion per gigawatt and 9–10 committed 2027 gigawatts, analyst math suggests Broadcom AI revenue 2026‘s $100 billion 2027 target is potentially conservative. The VMware software engine adds $20+ billion in ARR growing at 20%+ annually. Apollo and Blackstone’s $35 billion financing signal institutional validation. Street consensus: 36 Buy, 7 Outperform, 3 Hold — mean target ~$475, implying meaningful upside from current ~$413 levels.

Bear Case — Concentration Risk Is Real

The top three customers — Google, Anthropic, and Meta — account for approximately 70% of Broadcom AI revenue 2026 and the 2027 pipeline. If two of these three simultaneously slow their XPU ramp, the $100 billion target breaks. The OpenAI snag shows that even committed deals can hit financing complications. And Marvell’s multi-customer expansion means Broadcom’s 70% custom ASIC market share will likely erode through 2028.

The Next Catalyst — June 3, 2026 Q2 Earnings

The next time Broadcom management can address the OpenAI snag publicly and confirm the Q2 AI revenue guidance of $10.7 billion is the June 3, 2026 Q2 earnings call. If Q2 AI revenue meets or exceeds $10.7 billion — confirming the five other customer ramps are on track — the OpenAI situation is isolated and the $100 billion 2027 target remains credible. That June 3 call is the most important near-term event for the Broadcom AI revenue 2026 investment thesis.

Conclusion

The Broadcom AI revenue 2026 narrative is simultaneously the most compelling and most scrutinized story in the semiconductor sector. $8.4 billion in Q1, $10.7 billion guided for Q2, six XPU customers with committed gigawatt deployments, a $73 billion backlog, and a CEO who has explicitly stated “line of sight” to $100 billion in 2027 AI chip revenue alone — this is not a speculative story. It is one of the best-supported fundamental theses in enterprise technology investing.

The OpenAI Project Nexus financing snag is a legitimate risk that deserves monitoring. But it is a risk around Broadcom’s sixth and newest customer — not its largest, not its fastest-growing, and not the one that anchors the 2027 target. The five customers that do anchor it — Google, Anthropic, Meta, and two unnamed others — are all on track, all backed by $700+ billion in committed hyperscaler AI capex, and all deploying infrastructure at a pace that makes Broadcom AI revenue 2026‘s $100 billion 2027 target not just achievable but potentially conservative.

The June 3 Q2 earnings call will be the definitive near-term test. Until then, Broadcom AI revenue 2026 remains the clearest structural beneficiary of the AI infrastructure buildout — a two-engine business running at full speed in a sector where demand is structurally assured for years.

📊 Oplexa Report: Custom ASIC Market 2026–2033: $118 Billion Opportunity — $1,499

Full Broadcom competitive positioning, XPU customer pipeline, Marvell threat model, market share projections 2026–2033, and institutional investment framework for the custom AI chip market.

Frequently Asked Questions — Broadcom AI Revenue 2026

What is Broadcom’s AI revenue in 2026?

Broadcom’s AI revenue in Q1 fiscal 2026 was $8.4 billion — a 106% year-over-year increase driven by custom AI accelerator (XPU) demand and AI networking chips. Q2 FY2026 guidance is $10.7 billion, putting Broadcom on a $42.8 billion annual AI revenue run rate by mid-2026. CEO Hock Tan has guided 2027 AI chip revenue in excess of $100 billion, supported by a $73 billion backlog from six confirmed XPU customers.

Is Broadcom’s $100 billion AI revenue target for 2027 realistic?

Yes — analyst math supports the $100 billion target and suggests it may be conservative. At $20 billion per gigawatt (Bank of America estimate) and 9–10 committed gigawatts in 2027 across Google, Anthropic, Meta, and OpenAI, the implied revenue is $180–200 billion. The primary risk is customer concentration: if two of the top three customers slow their XPU ramp simultaneously, the target is at risk. The June 3 Q2 earnings call will be the first opportunity to confirm the trajectory post-OpenAI snag.

What is Broadcom’s OpenAI Project Nexus deal?

Project Nexus is Broadcom’s $18 billion custom AI chip buildout with OpenAI, targeting 10 gigawatts of compute before 2030. The snag: Microsoft refused to provide purchase guarantees needed to secure financing, creating timeline uncertainty for the planned H2 2026 chip delivery and 1 gigawatt 2027 deployment. OpenAI is Broadcom’s sixth and newest XPU customer. CEO Hock Tan confirmed the customer relationship remains intact — the issue is financing mechanics, not technical or strategic.

Who are Broadcom’s six AI chip customers?

Broadcom has confirmed six major XPU customers: Google (TPU v7 Ironwood and TPU v8), Meta (MTIA accelerators, multiple gigawatts from 2027), Anthropic (1 GW in 2026, 3+ GW in 2027), and OpenAI (first XPU targeting 1 GW in 2027). Two customers remain unnamed — industry analysts most frequently identify Apple and ByteDance as candidates.

How does Broadcom AI revenue compare to NVIDIA?

NVIDIA’s data center revenue was $35.6 billion in its most recent fiscal quarter — approximately 4x Broadcom’s $8.4 billion Q1 FY2026 AI semiconductor revenue. However, Broadcom’s 106% YoY AI revenue growth exceeds NVIDIA’s 93% data center growth, and the $100 billion 2027 target would make Broadcom’s AI chip business roughly 30% of NVIDIA’s current revenue scale — a dramatic shift. The two companies address different segments: Broadcom designs custom ASICs for specific hyperscaler workloads, while NVIDIA sells general-purpose GPUs across all customers.

Is AVGO stock a buy given the $100B AI target?

Street consensus as of May 2026 is strongly positive: 36 Buy ratings, 7 Outperforms, 3 Holds, no Sells per TIKR. Mean price target is approximately $475 versus current ~$413 levels. Bull case: $100B+ 2027 AI target supported by $73B backlog, VMware ARR growing 20%+, and Apollo/Blackstone $35B financing signal. Bear case: customer concentration in top 3 customers, OpenAI snag as potential bubble signal, and Marvell competitive expansion. This is not investment advice — consult a financial advisor before making any decisions.

Related Oplexa Coverage:

- Custom ASIC Market 2026: Why Hyperscalers Are Ditching NVIDIA — The structural shift that drives all six of Broadcom’s XPU customer relationships

- Meta-Broadcom AI Chip Deal 2026: 1 Gigawatt MTIA Deployment — Deep dive on Broadcom’s third-largest XPU customer

- Google Cloud Next 2026: TPU v8 and Broadcom’s Role — Google is adding Marvell as a third chip partner — competitive threat context

- NVIDIA $5 Trillion Market Cap: What Happens Next — How Broadcom custom ASICs fit into the GPU competitive landscape

- Amazon Trainium 3: The $225B Chip Bet — Marvell’s role in Amazon’s custom chip vs Broadcom’s ASIC model

- AI Data Center Power Crisis 2026 — Infrastructure constraints limiting the pace of XPU deployment

📊 Oplexa Report: Custom ASIC Market 2026–2033 — $1,499

Broadcom XPU customer pipeline, Marvell competitive threat model, custom AI chip market share projections, and 7-year institutional investment thesis for the $118B ASIC opportunity.

📊 Oplexa Report: NVIDIA Strategic Inflection Analysis 2025–2035 — $2,500

Broadcom vs NVIDIA custom ASIC competitive analysis, market share displacement model, and 10-year GPU vs ASIC investment framework.

📊 Oplexa Report: AI Chip Market Analysis & Forecast 2025–2035 — $1,499

Full semiconductor market cap projections, Broadcom revenue model by customer, NVIDIA vs custom ASIC market share trajectory, and AI chip investment thesis for institutional allocators.