By Mitthan Meena | Oplexa Insights

April 2026 | 11 Min Read

Five years. One contract. And a message to every chip company in the world: Google is not going back to general-purpose GPUs.

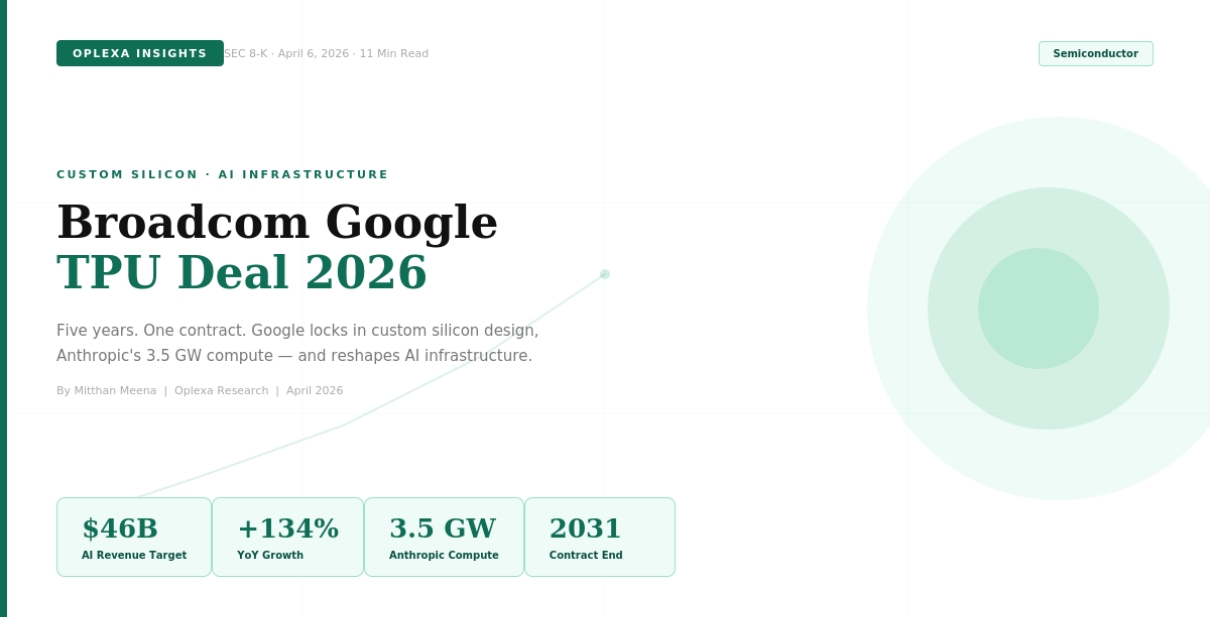

On April 6, 2026, Broadcom filed an 8-K with the SEC that confirmed the Broadcom Google TPU deal 2026 — a long-term agreement to design and supply future generations of Google’s custom Tensor Processing Units, along with a supply-assurance commitment for AI rack networking components, both running through 2031.

No headline valuation. Just a five-year locked roadmap that signals, with unusual clarity, where the $600 billion AI infrastructure buildout is going and who is going to supply it.

Broadcom shares climbed 3.65% in next-morning trading. And inside every custom ASIC program at every hyperscaler, strategy teams started recalibrating their own timelines. Here is what the Broadcom Google TPU deal 2026 actually means — for Broadcom, for Google, for Anthropic, and for the future of AI chip competition.

What the Broadcom Google TPU Deal 2026 Actually Says

SEC 8-K filings are legal documents, not press releases. They reveal facts, not narratives. And the facts in Broadcom’s April 6 filing are more consequential than the headlines captured.

The filing discloses two distinct agreements:

- A long-term agreement to develop and supply future generations of Google’s custom TPUs — covering successive TPU programs through at least 2031.

- A supply-assurance agreement for networking and other components to be used in Google’s next-generation AI racks, also running through 2031.

The second agreement is as important as the first. Custom AI accelerators do not operate in isolation. They require high-speed interconnects, power delivery systems, and rack-level infrastructure that must be co-designed alongside the compute die. Broadcom’s Tomahawk and Jericho network switch families already underpin a significant share of hyperscale AI networking. This supply-assurance clause locks Broadcom into Google’s full infrastructure stack — not just the silicon.

The Broadcom Google TPU deal 2026 is the first documented written agreement confirming that Broadcom’s engagement with Google covers not just individual TPU revisions, but a long-term secured roadmap for both computing and networking infrastructure through the end of the decade.

What the filing does not disclose: a dollar value. The contract amount is not specified. But Broadcom’s own revenue trajectory — and Mizuho analyst estimates that followed the earnings call — fill in that gap with enough precision to make the strategic picture clear.

The Numbers Behind the Agreement

Broadcom’s AI revenue trajectory has accelerated sharply over the past four quarters:

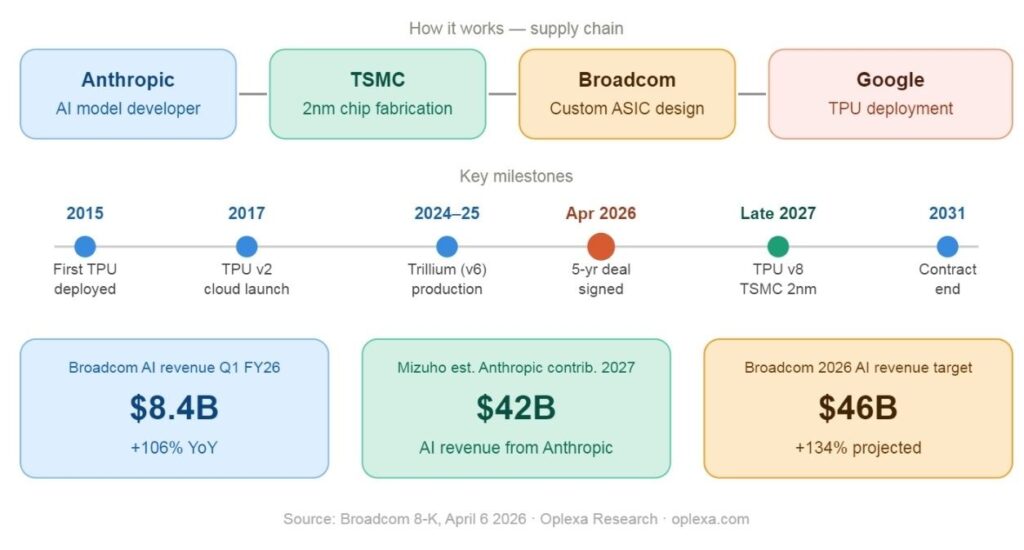

| Broadcom AI Revenue Q1 FY26

$8.4B +106% year-over-year |

Q2 FY26 AI Guidance

$10.7B Semiconductor segment only |

Projected 2026 AI Revenue

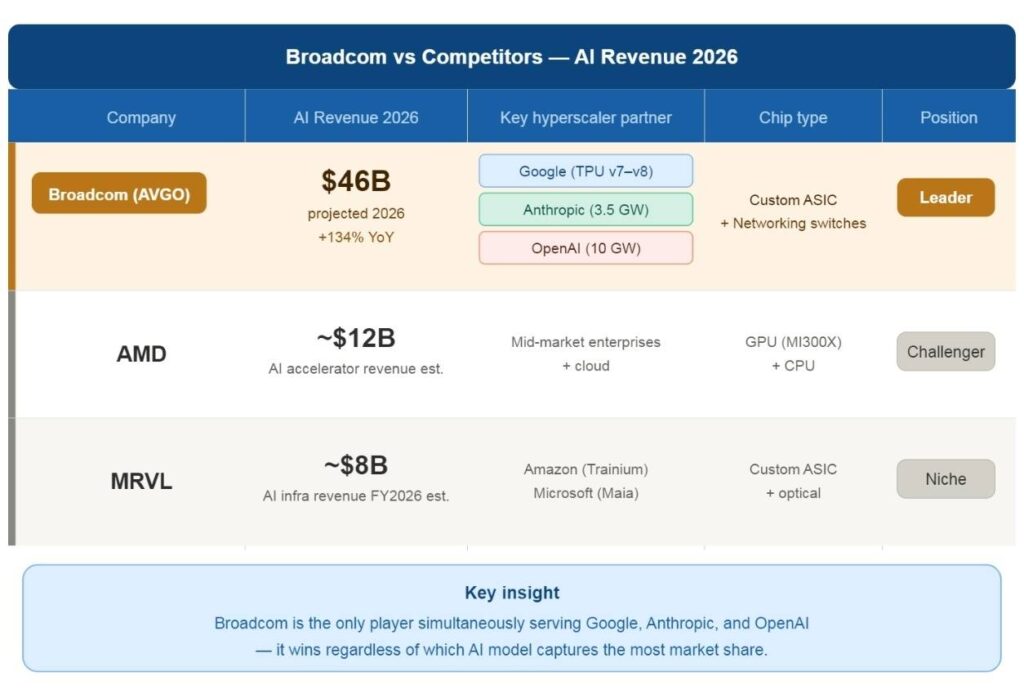

$46B +134% YoY projected |

The company’s stated target is $100 billion in AI chip revenue by 2027 — a goal that depends heavily on sustained Google TPU volumes continuing to grow at current rates. The Q1 FY26 print of $8.4B already represents more than double the $4.4B Broadcom reported in Q2 FY2025.

Mizuho analysts estimated that Broadcom would record $21 billion in AI revenue attributable to Anthropic in 2026, rising to $42 billion in 2027. These figures were published before the full Broadcom Google TPU deal 2026 scope was disclosed — revised estimates post-announcement will be materially higher.

What Broadcom Actually Does in the TPU Supply Chain

Understanding the strategic weight of this agreement requires understanding exactly where Broadcom sits in the TPU supply chain — because it is not where most coverage implies.

Google owns the TPU architecture and the software stack. Broadcom does not design the compute logic. Instead, Broadcom performs the silicon implementation: converting Google’s architecture into a manufacturable ASIC layout, supplying the high-speed SerDes interconnects, managing power delivery, and handling advanced packaging. TSMC handles fabrication.

That translation layer is where the margin, the complexity, and the strategic value actually live. No amount of architectural brilliance produces a working chip without a partner who can implement it at production yield across thousands of wafers. Broadcom has spent decades building exactly that capability.

| Component | Detail | Timeline |

| Custom TPU Design | Full ASIC implementation, SerDes, power management, packaging for Google TPU v7 and v8 generations | Through 2031 |

| AI Rack Networking | Supply assurance for networking and rack components in Google’s next-gen AI infrastructure | Through 2031 |

| TPU v8 Roadmap | Codenamed Sunfish (training) and Zebrafish (inference) — targeting TSMC 2nm in late 2027 | Late 2027 ramp |

| Anthropic Compute | 3.5 GW of next-gen TPU-based compute capacity for Claude model development | Starting 2027 |

TPU v8: Sunfish, Zebrafish, and the 2nm Transition

The most technically significant dimension of the Broadcom Google TPU deal 2026 is the TPU v8 roadmap. The next-generation TPU program features two variants built for different workloads.

TPU v8 Sunfish is the high-performance training variant. Broadcom has secured the design partnership for this configuration — the most demanding implementation in terms of memory bandwidth, compute density, and thermal envelope.

TPU v8 Zebrafish is the inference-optimized variant. MediaTek has secured a design partnership for this configuration. This is a deliberate strategic decision by Google — not an accident. Google is deliberately introducing competition among its ASIC design partners, using MediaTek’s cost-effective positioning to pressure Broadcom to reduce its premium pricing for training workloads.

Both Sunfish and Zebrafish are expected to be among the first chips to leverage TSMC’s 2nm process node in late 2027, delivering approximately 10–15% performance-per-watt improvement over 3nm at comparable die sizes.

For Broadcom, holding the training workload means holding the most technically complex and highest-margin portion of the TPU program — areas where Broadcom’s legacy in networking and SerDes provides structural advantages that MediaTek cannot easily replicate.

Anthropic Enters the Picture — And the Scale Is Enormous

The Google-Broadcom TPU agreement was disclosed alongside a separate but structurally related announcement: Anthropic has secured approximately 3.5 gigawatts of next-generation TPU-based AI compute through Broadcom, beginning in 2027.

One gigawatt of AI compute capacity, sustained continuously, is roughly equivalent to the entire AI compute fleet that Anthropic had access to at the beginning of 2026. The 3.5 GW figure — in addition to the 1 GW already coming online in 2026 — represents a 4.5x expansion of Anthropic’s compute base within 18 months.

The Anthropic revenue trajectory that drove this decision

Anthropic’s annual revenue run rate has surpassed $30 billion — up from approximately $9 billion at the end of 2025. That is a 3x increase in roughly 12 months, driven by explosive enterprise adoption of Claude and growing API consumption from developers building on the Claude platform.

Against that revenue trajectory, a multi-gigawatt compute expansion is not aggressive — it is conservative. The Broadcom Google TPU deal 2026 is the infrastructure backbone enabling this expansion: Broadcom supplies the silicon, Google provides the TPU architecture, and Anthropic gets the compute capacity to serve a customer base growing at triple-digit rates.

This is not a platform shift. Anthropic is not abandoning AWS. It is building a multi-cloud, multi-silicon compute strategy at a scale no startup has previously attempted — and Broadcom is the implementation partner across two of the three legs of that strategy.

What the Mizuho estimates imply

Mizuho’s $21 billion in Broadcom AI revenue attributable to Anthropic in 2026, rising to $42 billion in 2027, is a remarkable set of numbers. For reference, Broadcom’s total AI semiconductor revenue for all of FY2025 was approximately $12–13 billion. The Anthropic contribution alone, if Mizuho’s estimates prove accurate, would represent a doubling of Broadcom’s entire prior-year AI chip revenue.

The Competitive Landscape: Nvidia, AMD, and the Custom ASIC Race

NVIDIA’s position

NVIDIA remains the dominant supplier of AI training and inference compute across the industry. Its Blackwell architecture, and the forthcoming Rubin generation, continue to deliver performance improvements that custom ASIC programs struggle to match for general-purpose workloads.

But the hyperscaler dynamic is not about beating Nvidia on a benchmark. It is about cost structure, supply chain control, and performance per dollar at scale. At 10 billion inference requests per day on a fixed model architecture, a 30% improvement in performance-per-watt on a custom ASIC translates directly to hundreds of millions of dollars in annual operating cost savings.

The OpenAI parallel

Broadcom’s position as the implementation layer for Google’s TPU program is mirrored by its separate 10 GW custom silicon co-development program with OpenAI, announced in October 2025. Broadcom is now the hardware partner for two of the three largest frontier model developers in the United States.

This positioning gives Broadcom what no other semiconductor company currently has: structural exposure to AI model training and inference demand across multiple competitive AI ecosystems simultaneously. Broadcom does not need to pick a winner — it supplies the infrastructure that all the competitors run on.

AMD and the inference opportunity

AMD’s MI300X series has carved out a credible position in AI inference. But AMD’s strategic challenge is that its general-purpose accelerator model faces the same structural headwinds as Nvidia’s at the hyperscaler level. AMD increasingly competes for the mid-tier: enterprises and AI-native companies that do not yet have the scale to justify a custom chip program.

What This Means for the Semiconductor Market in 2026

The custom ASIC market inflection is confirmed

Oplexa’s March 2026 analysis projected that ASIC shipments would surpass GPU shipments for the first time in history by 2028. The Broadcom Google TPU deal of 2026 is a structural validation of that trajectory. No hyperscaler signs a five-year locked supply agreement for infrastructure it plans to walk away from.

The TSMC capacity question

Both TPU v8 Sunfish and Zebrafish target TSMC’s 2nm node in late 2027 — placing them in direct competition for advanced node capacity alongside Apple’s A-series chips, AMD’s next-generation processors, and Nvidia’s Rubin architecture. TSMC’s 2nm capacity allocation will be one of the most strategically contested resources in the semiconductor industry over the next 24 months.

The MediaTek signal

The TPU v8 Zebrafish partnership between Google and MediaTek should be read as Google deliberately seeding a lower-cost alternative for inference workloads. For Oplexa clients tracking the semiconductor competitive landscape in Asia, the MediaTek engagement is the thread to pull. If Zebrafish ships on schedule and performs to spec, it validates MediaTek as a credible custom ASIC design partner — with implications for every hyperscaler evaluating diversified chip-design partnerships.

Conclusion

The Broadcom Google TPU deal 2026 is not a supply contract. It is a statement about the architecture of AI infrastructure for the rest of this decade.

Google is not buying chips. It is locking in the design, implementation, and supply-assurance layer for its entire AI compute stack. Broadcom is the indispensable translation partner between Google’s architectural intent and the physical silicon that runs Gemini, serves Google Cloud, and — through the Anthropic side agreement — increasingly runs Claude. Unlike Nvidia H100 GPU-based deployments, the Broadcom Google TPU Deal 2026 reflects a shift toward custom silicon — a Capital Expenditure commitment that locks in AI infrastructure for the rest of the decade.

The numbers are large enough to reshape Broadcom’s revenue profile, redefine what a semiconductor company’s AI exposure looks like, and set the competitive baseline that every other custom silicon program will be measured against.

For anyone tracking where AI infrastructure buildout value actually lands, the Broadcom Google TPU deal 2026 is the clearest signal yet. Not for what it announces — but for what it permanently confirms.

Related Research from Oplexa